So, What Is NYDFS 23 NYCRR 500?

It’s a set of cybersecurity requirements created by the New York Department of Financial Services. If you're a bank, insurer, lender, or really any financial services company under NYDFS oversight, this applies to you.

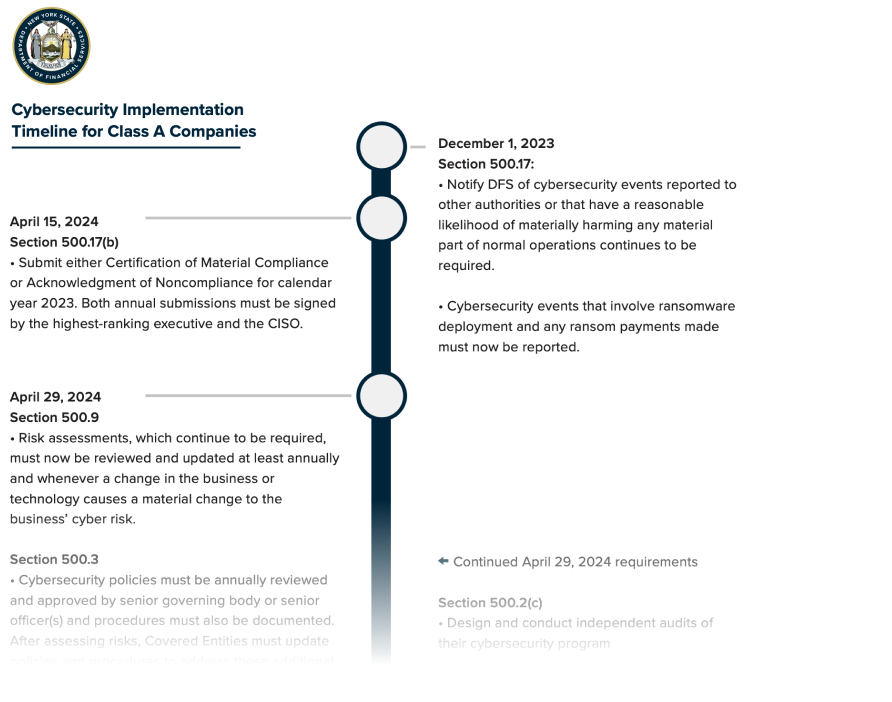

This is not a new mandate; it’s been around since March 1, 2017. Most of the core rules were enforced within the first year or two. Since then, new updates have been layered in. The latest batch landed in November 2023, with new deadlines running through 2024 and into 2025.

How Does It Compare to Other Cyber Laws?

There’s definitely some overlap. But the details and the tone are different.

GDPR (Europe): Both care about breach reporting and personal data. GDPR gives you 72 hours to report a breach, and NYDFS does too, at least in certain cases. But GDPR is wide-reaching, covering every industry in the EU. NYDFS is laser-focused on finance.

CCPA (California): CCPA is more about what individuals can do with their data, see it, delete it, or opt out. It’s consumer-centric. NYDFS is more technical. It tells institutions how to protect data, not just what rights people have over it.

HIPAA (Health Insurance Portability and Accountability Act): Similar concerns in terms of risk assessments and protecting sensitive information. But NYDFS goes further. It tells you to appoint a CISO, test your systems, encrypt, and manage vendor risk. HIPAA doesn’t get that specific.

So yes, the NYDFS regulation shares themes with these, but it’s more prescriptive and focused on financial services.

What’s Different About It?

Here’s where it really starts to stand out.

It starts with risk. You don’t just build a generic cybersecurity plan. You assess your actual risks and tailor everything around that.

You need a CISO (and we hope you already have one). Not someone juggling multiple roles. A dedicated Chief Information Security Officer. That’s baked into the requirement.

There are concrete controls. Things like multi-factor authentication, encryption, and regular testing. These aren’t nice-to-haves; they’re spelled out in black and white.

Third-party risk matters. You’re responsible not just for your own systems, but also for what your vendors are doing (or not doing).

2023 Updates:

- 24-hour notice if you pay ransomware.

- Annual board certification of compliance.

- Independent audits for larger institutions.

- Expanded CISO responsibilities and direct reporting lines.

It’s not vague. It leaves little room for interpretation. That’s both the value and the challenge.

What’s the Status Right Now?

The regulation is fully active. Most of it has been for years.

What’s new are the amendments introduced in 2023. These added tighter breach notification timelines, expanded the CISO’s role, and introduced new reporting expectations. That's where you need to pay more attention to!

Some of those deadlines are already here. Others stretch into 2025. If you haven’t looked at it recently, now might be a good time.

You can find the official updates on the NYDFS site at dfs.ny.gov, but fair warning, it’s not exactly a light read.

Why Does It Matter?

Many companies view regulations like this and think, "We’ll deal with it if we have to."

But here’s the problem. When a breach happens and you’re not in compliance, the fallout isn’t just fines. It’s public trust. Brand damage. Lost customers. Internal chaos.

The regulation is there to help you avoid a worst-case scenario.

Think of it as your cybersecurity floor, not the ceiling.

So, What Should You Do Next?

Start simple.

- Pull up your cybersecurity plan and see how it maps to NYDFS requirements.

- Make sure someone owns this - ideally, your CISO, if you have one.

- Pay extra attention to breach reporting, vendor oversight, and system testing.

And if you’re not sure where you stand, don’t wait for an audit or a breach to find out. This isn’t the kind of thing that’s easy to fix after the fact.

Even if you feel mostly covered, there’s probably something in the 2023 updates that needs attention.

Orchid helps organizations stay ahead of NYDFS requirements by offering targeted visibility into how identity is actually managed across their environment. Customers can select NYDFS as a compliance framework, and Orchid automatically analyzes their application stack to detect potential violations, whether it's missing multi-factor authentication, weak encryption, or unmonitored third-party access. Instead of relying on outdated inventories or manual audits, Orchid gives teams a clear, up-to-date view of where they stand and what needs fixing. So when regulators call, you’re not scrambling. You already know. See for yourself—request a personalized demo to learn more.